Should Warren Buffett Dismantle Berkshire Hathaway?

The Raison D’etre For the Company May No Longer Exist

2020 should have been a banner year for Berkshire Hathaway (NYSE: BRK-B). In previous crises or market plunges, Berkshire has been swift in making savvy investments, swooping in when investors were frightened and seeing value where others could not.

But 2020, has not turned out that way. The leadership of the company including its Chairman and CEO, Warren Buffett, has been plagued by inaction and confusing decisions. What is going on with the greatest investor of all time and his company?

The first real head scratcher came when Berkshire didn’t buy any of its own shares or make any sizable investments during the panic lows of the market in March and April.

Then followed a series of baffling decisions.

1. Bailing on airline stocks at the low

2. Inexplicably holding on to Wells Fargo

3. Then later in the year, selling Wells Fargo

4. Not buying back its own stock at $170 per share

5. Then buying back shares later in the year when the stock was over $200 per share

Then came the Snowflake (NASDAQ: SNOW) investment, which by itself wasn’t confusing. But why did Berkshire agree to invest at whatever the Snowflake IPO price was set at after allowing the Berkshire name to be marketed as part of the IPO? For Snowflake to use Berkshire’s brand to price the IPO at a higher price all but ensured that Berkshire would pay a higher price for its investment. I’ve never seen Berkshire purposively pay a higher price.

It’s clear that the Snowflake investment was not led by Buffett, but by probably one of his proteges and now we start knocking on the door of what is wrong with Berkshire. And there are numerous problems.

Berkshire’s investments are now handled by three people, Warren Buffett, Ted Weschler and Todd Combs. Maybe there are too many cooks in the kitchen. I think this creates a confusing situation with no apparent rhyme or reason to making investments, other than, “hey these are smart, patient investors.”

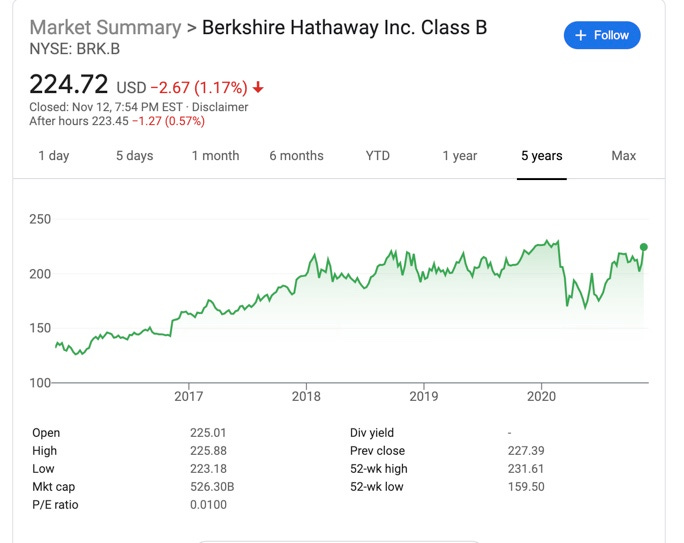

Berkshire’s size is also enormous. It now has over a $500 billion market cap. The types of investments it can make that really move the needle are much more limited than in the past. And the sheer complexity and range of its businesses and investments make analyzing it, much less leading the company, no easy task.

But the biggest problem is that Berkshire’s raison d’etre, its reason for being and thriving, no longer exists. Berkshire thrived in an environment that was short patient capital, where there were many opportunities to capitalize on mis-priced large cap stocks, when government inaction or slow responses meant many companies had nowhere else to turn for financial help and when there were fewer financial buyers of large private and public companies.

Unfortunately, none of those conditions exist today. The world is awash in capital, with plenty of long-term capital available. There are multiple financing options and exit routes that both private and public companies have as options. And most importantly, government has become much more active and responsive in financial crises and in downturns than in the past. The government action during COVID was so swift, that Charlie Munger (the executive Chairman of Berkshire Hathaway and its vice chairman) was quoted as saying that their phone was not ringing, meaning no one was calling Berkshire for financial help.

And think about the reasons people invest in Berkshire Hathaway? First, they probably do it for Warren Buffett and Charlie Munger. Buffett is 90 and Munger is 96. What happens when they are gone?

Warren Buffett has proven he is still absolutely capable of knocking it out of the park as an investor with his Apple (NASDAQ: AAPL) investment making an astonishing $80 billion on its investment from his purchase in 2016-2018, but how much longer will he be in charge?

And I don’t need Berkshire Hathaway to invest in tech stocks like Snowflake. I would rather invest with Brad Gerstner’s Altimeter Capital or Altimeter’s most Special Purpose Acquisition Corporation (NASDAQ: AGCUU), or any number of other investors who are experts in the technology field.

What’s worse is that investors are no longer giving Berkshire the benefit of the doubt or credit for its investment prowess. Its stock is basically flat over the last three years. And even its Apple investment bonanza is not translating to its stock price. Why?

The Berkshire story is now the narrative of a complicated conglomerate with aging leadership. In my experience, companies or investments that become complicated start getting discounts to their intrinsic value and start underperforming, until a catalyst comes along to simplify the story.

Warren Buffett has not only compiled one of the great investment records of all time, but he very clearly changed the investment landscape, influenced countless investors, and business leaders as well as helped shape the modern business world. Unfortunately, it looks like Buffett is now a victim of his own success. Berkshire is too large, too cumbersome with too few opportunities going up against an avalanche of capital and competitors.

Maybe, Buffett’s final act will be to surprise everyone and dismantle his creation in one last giant act of creating incredible value for his investors…