A Vireo Strong Quarter

Vireo Reports the Strongest Q4 Earnings in Cannabis

Only in cannabis can a company report 11.3% same-store sales growth, beat estimates by over 10%, lay out a roadmap to double revenue—and still get a collective shrug from investors. Well, at least from the few investors still paying attention.

This week, Vireo (OTC: VREOF) reported a phenomenal quarter: $105 million in revenue, up 25% on a pro forma basis. Most importantly, this growth came at a time when many cannabis companies are struggling to grow at all.

The company’s outperformance was evident even in mature markets. In Nevada, Vireo grew sales 12% while the overall market grew just 2%. In Missouri, it grew 7% versus 2% for the market.

This sends a strong signal: Vireo is not just a Minnesota story or a roll-up strategy. The company is demonstrating it can execute and grow in highly competitive markets post-acquisition.

Minnesota Drives a Strong Forward Outlook

Vireo is nearing completion of its new indoor facility in Minnesota, which will significantly increase supply. CEO Jon Mazarakis noted that the market is likely to remain supply-constrained for years.

Our channel checks support this view. One private operator recently said they expect to be “sold out for the foreseeable future.” Despite being months from completion, this cultivator has already received overwhelming demand from retailers—some even willing to put down deposits to secure product.

Acquisition Train Continues Full Steam Ahead

Vireo is in the process of closing four acquisitions that could add over $400 million in annual revenue, all at valuations well below 5x EBITDA.

Once completed, the company could reach $800–$900 million in revenue, making it one of the five largest cannabis companies globally. We anticipated this trajectory last year, but the speed of execution has exceeded even our expectations.

We also expect meaningful synergies—particularly in Colorado, where the company could approach $200 million in revenue from a single state. When asked about future acquisitions, CEO Mazarakis (“Maz” in the industry) said, “We will never be done in Colorado.” We suspect that mindset extends well beyond Colorado.

Contrast with Other MSOs

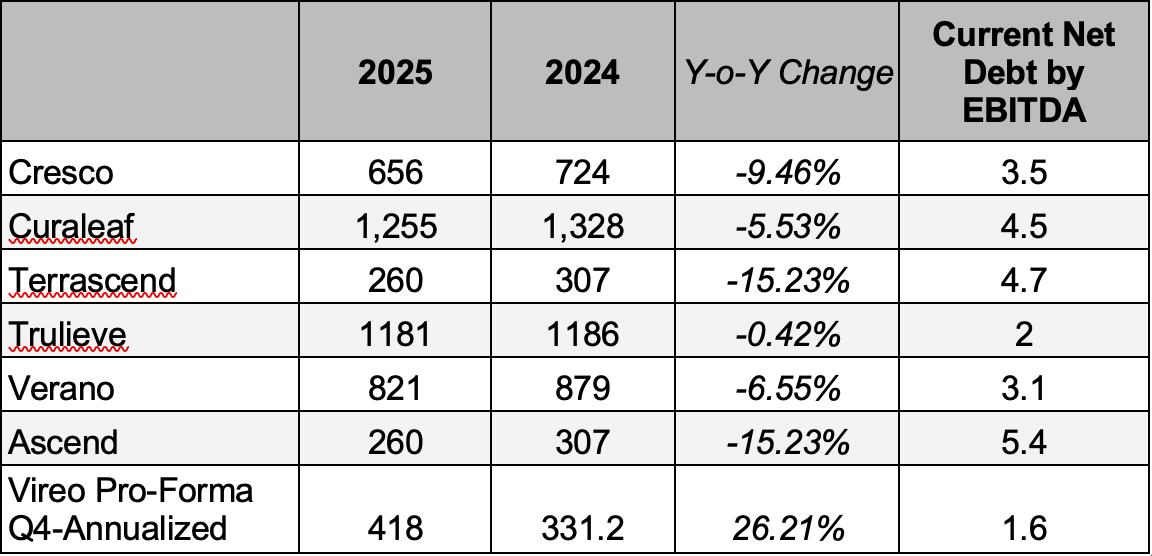

The contrast between Vireo and other Tier 1 MSOs (with the exception of Green Thumb) could not be more stark. While many competitors are reporting declining revenues, Vireo is delivering double-digit growth backed by a fortress balance sheet, including over $100 million in cash.

In 2026, Vireo is poised to be one of the few cannabis companies delivering meaningful revenue growth—alongside names like Grown Rogue and LEEF. In fact, if the company maintains its current acquisition pace, we believe it is on a trajectory to become the largest cannabis company in the world by revenue.

Yet the stock still trades at just 4–5x EBITDA. In our view, this disconnect reflects a lack of investor participation in the sector. With limited capital remaining in cannabis—and little new money entering without federal reform—companies like Vireo are being overlooked.

Consider this: if the largest cannabis-focused ETF, MSOS, was to rebalance based on Vireo’s growing scale, it could need to purchase anywhere from 200 to 400 million shares (The index has 0.5% of its assets in Vireo at the moment). Given the stock’s current liquidity, that level of buying is not feasible today. But looking ahead, as new capital enters the space, it is likely to concentrate in the largest and fastest-growing operators—which should include Vireo.

We remain excited by Vireo’s strategy and believe the stock is materially undervalued relative to its growth, scale, and execution.

We are still Vireo bullish.