HireQuest's Earnings Power Soars

HireQuest's Earnings Power Soars

The Mindset Value Fund Q1 2023 Investor Letter

Disclaimer: The below post is my Q1 2023 Investor Letter that I sent to investors in the Mindset Value Fund this week. This post is NOT a solicitation. I talk about stocks that I own and my view of the future. It is imperative that you do your own due diligence and not rely on anything written below. I’m posting this in order to show how my writing translates to actual performance. With that, I hope you enjoy and gain insights.

The Mindset Value Fund finished the first quarter up 16.8% on a net basis.

Three Stocks Drive Our Performance

Our performance in the quarter was driven by three companies, Consorcio Ara (Mexico: ARA), Glass House Brands (OTC: GLASF), and HireQuest (NASDAQ: HQI).

Consorcio Ara is ridiculously cheap, trading at a valuation of just 33% of book value and 27% of net asset value with net cash on the balance sheet. The stock rallied on improved sentiment about how Mexico will benefit from nearshoring and American tensions with China. We expect strong growth from ARA in the back of the half of the year and love collecting our 5% dividend while we wait for the Mexican housing shortage and positive demographics to collide.

Glass House Brands bounced back after a big SAFE Banking sell off in December after reporting a good first quarter, but more importantly improved guidance of being free cash flow positive in Q2 and continued progress of driving down COGS. The company has a clear and durable cost advantage over competitors that should only grow over time.

HireQuest’s Earnings Power Soars

But the company I really want to highlight is HireQuest, which is our largest position. We first bought HireQuest when it was trading below $7 per share, and I’m equally if not more excited about the company at around $20 per share, and I want to tell you why.

HireQuest is a staffing company for temporary day laborers, factory workers, dental hygienists, drivers and even executives. The key though is that instead of being a vertically integrated staffing company, HireQuest runs a franchise model. Over thirty years of experience has led founder/CEO Rick Hermanns and his team to develop what I believe to be a superior lean business model that he is using to roll up staffing companies that are either smaller mom-and-pop businesses or underperforming vertically integrated companies.

HireQuest’s business model is that they handle the accounts receivables that are owed to franchises, manage workers comp, and provide national accounts to the franchisees. The franchisees focus on matching temporary employees with employers. HireQuest can provide vast savings by having all the franchisees’ employees under one workers comp policy, much more than any small sub-scale company can.

To understand the HireQuest story and the accretive power of its model you only need to look at how the company came to be public. HireQuest was a thriving private company that took over a struggling and underperforming vertically integrated staffing company called Command Center, which was publicly traded. When you reverse engineer the merger financials, you realize that HireQuest was basically paid to go public. How? Well, it acquired Command Center and then turned around and sold off its branches as franchises, thus more than paying off the cost of the acquisition and then turned what was an inefficient staffing company into a lean and mean franchise business. I wrote about this in my original report about the company.

HireQuest was able to convert former branch managers of Command Center into franchise business owners and dramatically increase their income. For anyone with hustle and those willing to operate under HireQuest’s system, there was and still is a real opportunity to thrive. I believe the company’s system of incentives is superior and is the key to its success. I interviewed CEO Rick Hermanns about the company’s system of incentives.

The only question was whether the Command Center acquisition was a “one-off” acquisition or could it be duplicated. The company then followed this up with a series of very accretive acquisitions during COVID. And the company has continued acquiring underperforming or small, inefficient operators and converting them to their model.

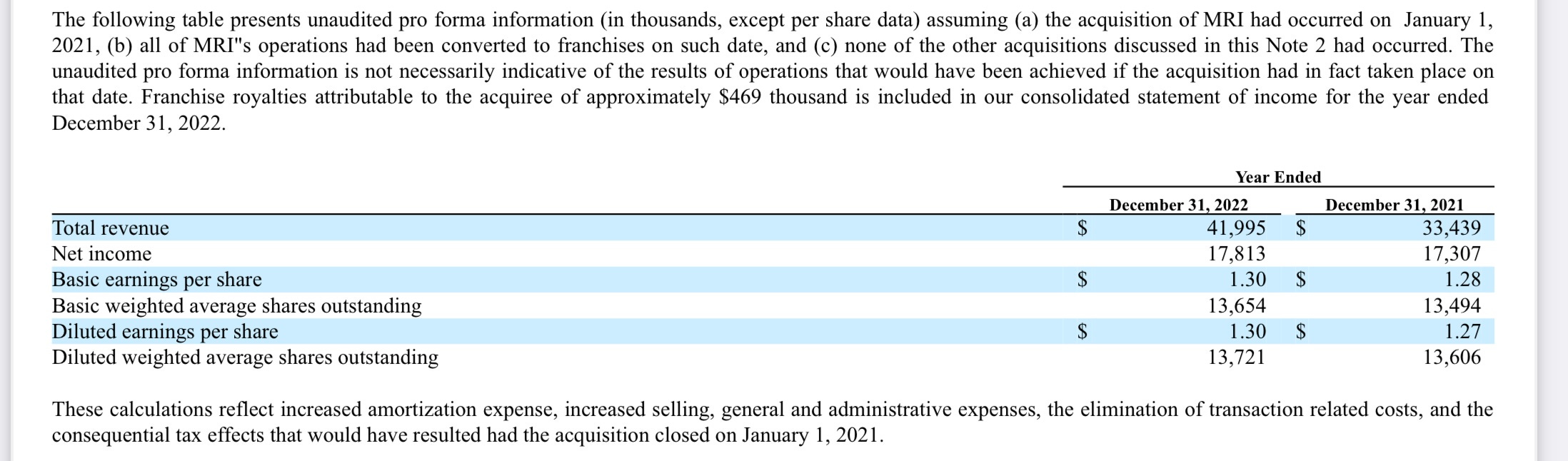

To highlight just how much value HQI can create when they are buying these companies, check out its recent MRI acquisition, which it closed in December. It’s important to note that HQI earned $0.91 per share in fiscal 2022.

So, I want to highlight a recent disclosure from the company’s latest 10k filed in March of 2023.

Imagine my surprise, upon reading that HireQuest would have earned $1.30 per share if the MRI acquisition had closed on January 1st, 2022, instead of December 2022. That’s almost $0.40 per share of accretion and that is before HireQuest goes to work to integrate the company, improve its system and actively work to make it more profitable.

This is one reason why I think HireQuest now has earnings power of $1.75 per share in earnings, almost all of which is free cash flow. This means HireQuest is trading at 11 times that earnings estimate. That multiple does not seem appropriate for a business with 60% operating margins and run by one of the best CEOs I’ve ever invested alongside of. It’s important to note that insiders own over 60% of the company and are aligned as fellow shareholders.

Another point to mention is that HireQuest earns a small percentage from its franchises who earn a small percentage from their temporary employees, so if there continues to be labor inflation, then HireQuest should benefit from that labor inflation.

Also consider that even though this is a cyclical business, if employment falls and/or we enter a recession, HireQuest gets stronger. Why? Because they finance accounts receivable. When the economy weakens, HireQuest’s accounts receivable balance falls and cash rises. And since their model is to acquire other staffing companies and to convert them to its best-in-class franchise model, cash goes up at exactly the time when valuations go down and companies may be looking for help or to be acquired.

A reminder of the strength of its model is that the company was profitable in the second quarter of 2020, when our economy came to a complete halt during COVID. If you can be profitable during a once in a lifetime shutdown of the economy, you have one hell of a business.

I believe the company is on its way to $2.50 to $3 per share in annual earnings. This is a business that needs little recurring capex as this is a service business, meaning that those earnings are pure free cash flow. While the stock may seesaw along with the market, it is building a free cash flow machine. What is that worth? I’m not sure, but I’m quite confident that it is not $20 per share. And with the right market conditions, this could easily trade at a 20 or 30 multiple.

Why Are We Still Invested in Cannabis?

Most cannabis stocks have been crushed. Funds are shutting down; analysts are leaving, and no one wants anything to do with the sector. At times like this, I think it is helpful to remember why our value fund is invested in cannabis.

Cannabis is an industry that does about $100 billion in revenue and could be on its way to $200 billion in revenue, due to the medicinal applications of cannabis. Thanks to the quirk in laws and conflict between Federal and State regulations, 99% of the smartest financial people in the world are not involved in the industry and thus there is no competition to research or to due diligence.

I was recently interviewed by AlphaSense about why I continue to believe the opportunity in cannabis is so extraordinary. You can find that interview here:

But let’s talk concrete examples. Consider Grown Rogue (Canada: GRIN) as a great example of the opportunity in cannabis. We invested in the company through a convertible debt deal that pays us 9% annual interest but allows us to convert into approximately 6% of the company. Grown Rogue is one of the most efficient indoor craft cannabis cultivators in the U.S., if not the world. My research shows that it is operational excellence that is in short supply, not limited licenses and that is what Grown rogue has mastered and gives it a competitive advantage.

Further, Grown Rogue is free cash flow positive in both Oregon and Michigan despite fierce competition and low cannabis prices. And the company is working on entering other limited license markets, all the while growing at more than 25% a year in the most competitive markets in the country.

I believe that if Grown Rogue can enter a few new markets, the company might be trading at TWO times estimated 2024 EBITDA. What other industry can we invest in a fast-growing company with durable cost advantages that generates free cash flow in an exciting growth market, get paid 9% interest and have the option to convert into the company at two times EBITDA?

This is why I’m so focused on the sector and why it should pay to continue to be invested in cannabis.

Summary

Not only is our portfolio driven by companies like HireQuest and Grown Rogue with growth and secular tailwinds, but remember we are invested in a host of securities that pay us dividends and interest including preferred equity, convertible debt, and a senior secured note that with existing dividends, gives our portfolio an annual yield of over 5%. This year has already started out on a different foot than last year, and we expect more positive news and strong growth from our investments as the year progresses.

Thank you as always for your support and for entrusting Mindset with your capital.

Sincerely,

Aaron M. Edelheit