Netflix is Over the Moon

While Disney Is Stuck in the Cave of Wonders

“That’s been one of my mantras – focus and simplicity. Simple can be harder than complex: You have to work hard to get your thinking clean to make it simple. But it’s worth it in the end because once you get there, you can move mountains.” Steve Jobs

Netflix’s (NASDAQ: NFLX) single-minded focus on its streaming platform is not only moving mountains it is taking the company over the moon. The company’s unwavering commitment to its strategy has taken the company to a market cap over $200 billion and 195 million global paying subscribers.

I was reminded of this focus when my family and I watched and enjoyed Netflix’s latest animated movie Over the Moon this past weekend. The movie was helmed by long time Disney (NYSE: DIS) animator Glen Keane (Little Mermaid, Aladdin and Beauty and the Beast). This was a well-made movie, despite a few plot holes and clearly copied elements from past Disney movies including the classic Disney trope in which one of the parents die. Netflix has to be over the moon at the reception (Rotten Tomatoes has it at 79% from critics and 81% from the audience).

As an investor (no position in either company right now), the minute the movie ended, my thoughts were racing about how Disney has a really big competitive problem. Disney (especially after acquiring Pixar) has dominated animated movies so thoroughly the last ten to twenty years that it seems inconceivable that anyone could challenge them.

From Frozen to Toy Story and Cars, Disney has produced stories, characters and films that have truly resonated with fans and especially children. This has resulted in outsized profits in the theaters and the after-market sales of DVDs, digital purchases and merchandise. This has also led to many families subscribing to Disney+ just to get access to the film library of Disney children classic movies.

And now here comes Netflix, which plans to come out with six animated films a year starting in 2022. Compare that to Pixar’s development pipeline of at most two animated films a year. And if they are anywhere near the quality of Over the Moon, Disney has a serious problem. Animated movies have been a major profit source for Disney. From the box office to DVD sales to rentals to now digital sales, Disney has generated billions in profits from this category. What exactly happens when Netflix gets consumers used to extremely high-quality animated movies for free as part of the Netflix subscription plan? Why would any parent take their kids to the movies and spend $50 to $100 once you include drinks and popcorn when that is almost the price of the basic annual Netflix subscription?

Further, in a more saturated market, it will be harder to stand out and thus could become a lot harder to create iconic animated characters, which has been Disney’s bread and butter.

But Disney’s biggest problem is not the new threat of Netflix’s animated movie ambitions. No, instead Disney’s biggest problem is that it has become an unwieldy, slow-moving, media conglomerate in a time when the competition is focused and fast.

Disney is Stuck in the Cave of Wonders

The media and entertainment assets of Disney are so sprawling that Disney may have a problem akin to Aladdin in the Cave of Wonders. There are so many treasures that Aladdin and his monkey, Abu, are overwhelmed and there is a strong temptation to grab all of the treasures.

Disney is currently struggling with multiple problems including the short term COVID impact to its theme park business and theatrical movie releases to declining ratings for ESPN, ABC and its old-line media networks. And then there is the quandary of what to do about Hulu. There have been some articles recently that Disney has no idea what to do with Hulu.

Meanwhile, Netflix keeps its head down and focuses on nothing but driving value for its streaming platform and growing its user base. All Netflix wants is the lamp, which houses the genie. Netflix only wants to dominate streaming.

Simplicity is simply a strategic advantage for Netflix. And Disney’s complexity puts it at a strategic competitive disadvantage.

I’m not the only one who sees problems with Disney. Activist investors are knocking on the door. Third Point’s Dan Loeb has a large stake in Disney and sent management a letter asking the company to hold off on resuming its dividend and instead spend it on content for Disney+.

Another long-term investor, respected investor Chris Bloomstran with Semper Augustus, fired back and defended the company, but also offered his options for Disney to consider.

I think both investors have good points but are potentially missing the bigger picture problem with Disney. Disney needs to simplify. While in the past it might have made sense to be a large media conglomerate and lump ESPN, Hulu, theme parks, movies and animation together, that is no longer the case. And its complexity seems to be actively hurting decision making at all levels of Disney.

How could Disney simplify? One option may be to spin off Disney’s old-line media empire in ABC, ESPN, and combine it with Hulu. This way those adult oriented assets can re-orient around streaming and effectively make capital allocation decisions that won’t compete with its Disney+ and theme park businesses.

While investors in Disney may envy Netflix’s valuation and giant market cap and question why Disney can’t be more like Netflix, I’ve always been attracted to Disney’s theme park business. Pre-COVID, this business is a one of kind, phenomenal business that truly has no competition. Disney’s theme parks generated almost $7 billion in operating profits in 2019, despite heavy infrastructure investment. It’s operating margins were almost 26%. This is a damn fine business.

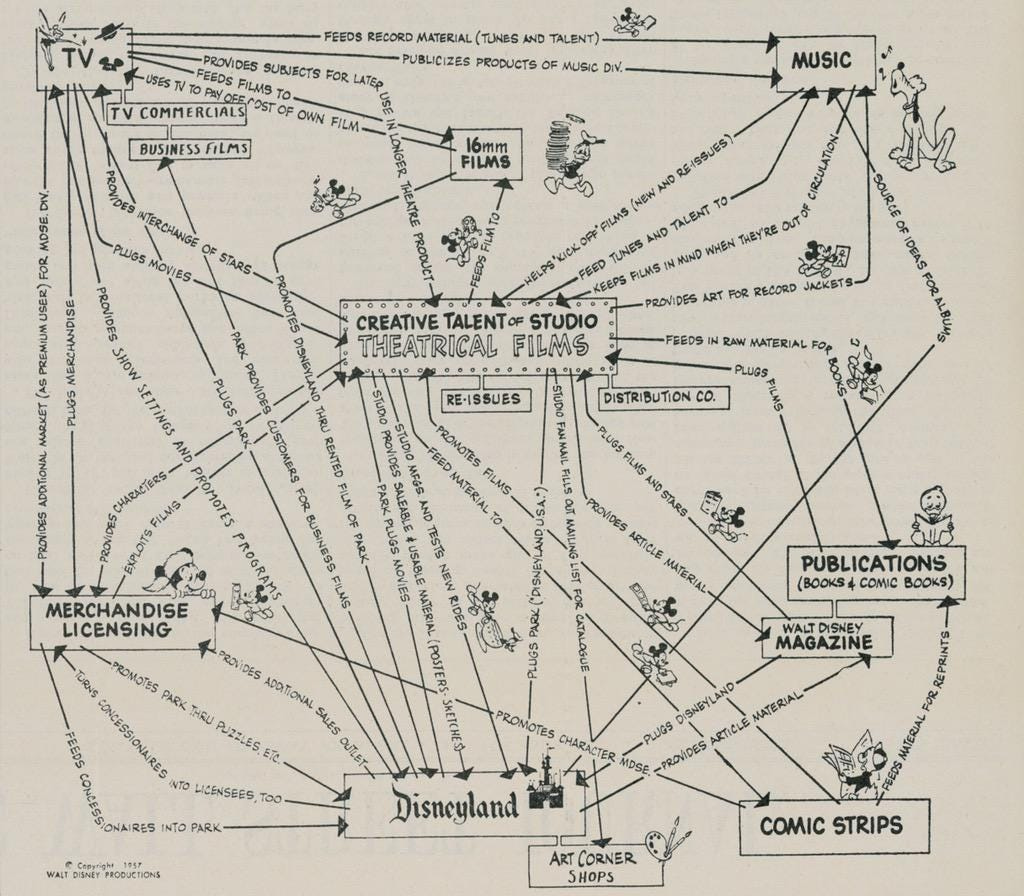

Disney has always thrived on the screen and in-person and this was part of Walt Disney’s original view of Disney’s ecosystem.

And this is exactly how Disney can effectively compete against Netflix and everyone else. Its theme parks are irreplaceable assets and when the virus is under control, Disney should double down on in-person experiences and merchandising and use Disney+ as an entry point into its ecosystem. Disney+ should simply be a CAC (Cost of Acquiring the Customer) for cruises, merchandise, and in-person experiences.

As long as Disney is slowed down by its complexity, it will not move as fast as it needs to in the current environment and it is likely to disappoint investors. I was a happy Disney shareholder before COVID, and I would love to be one again. But the company has to focus so they can escape the prison that is the Cave of Wonders.

P.S. I highly recommend you read Matthew Ball on Disney. This essay is a great introduction for why you should read what he writes: Disney as a Service.