Warning: The following column is about a microcap company. Microcaps by definition can be illiquid and experience wild gyrations. It is important to do your own due diligence, rely on your own research and understand that microcaps can be very volatile. Please proceed reading using your highest levels of caution. That being said…

Grown Rogue (Canada: GRIN, OTC: GRUSF) is one of the fastest growing and also one of the only profitable publicly traded cannabis companies that produces real free cash flow. And yet at the same time I think Grown Rogue is the most undervalued publicly traded cannabis stock. And even more, I believe the company’s performance and strategy is quite important to the future of the cannabis industry despite its seemingly insignificant $60 million market. I think the company should be analyzed and covered by research analysts despite its size.

The question is why do I believe this?

New Jersey is a limited license state, meaning the state purposely limits the number of companies that can participate in the industry. Further constricting the playing field are local rules and regulations, the combination of which leads to New Jersey having less than two dozen cultivators and only 64 dispensaries for a population of over 9 million people.

Remember that interstate commerce for cannabis is currently not allowed, so this limiting of licenses has led to poor to mediocre quality products for New Jersey consumers, but more importantly very high cannabis prices. While the average wholesale cannabis price hovers around $1000 a pound nationally, in New Jersey it is currently almost triple that price.

But this is about change as Grown Rogue announced today they are entering New Jersey (Please note that the timing of the entry is dependent on some final regulatory approvals). Grown Rogue has the #1 flower by market share in Oregon, an unlimited license state with exceptionally high standards for quality and genetics. And the company also is in the top 5 in Michigan, another very competitive state.

I have written about Grown Rogue after my first investment in the company, posted an interview with the CEO Obie Strickler and posted a follow-up interview about their strategic partnership with Goodness Growth.

But most importantly, I’ve written that the big myth in cannabis is that growing high quality cannabis, consistently at scale is somehow easy. Cannabis cultivation at scale is actually really, really difficult. That is why I have been focused on companies that show operational excellence like Grown Rogue. I believe it is operational excellence that is in short supply in cannabis, not limited licenses.

For Grown Rogue, the entry into New Jersey is a potential grand slam and the beginning of a much bigger expansion into multiple limited license markets with their Oregon-quality flower. Why?

Because Grown Rogue not only makes great cannabis that consumers love, but they do it at an almost unbeatable cost. I believe that Grown Rogue is one of the most efficient indoor producers in the country with an all-in cost of less of less than $600 a pound. I believe this cost is at least 40% and most likely more than 50% what it costs larger publicly traded cannabis companies to produce cannabis flower.

This means that the company is free cash flow positive at $800-$900 flower pricing in Oregon and Michigan. The company is so efficient that it boasts some of the highest margins in the industry despite being in the most competitive markets. They announced 33% EBITDA margins in their last quarter (along with 48% revenue growth).

So, what happens when they enter a market with $3000 and not $800 pricing? Well, I don’t think that kind of pricing is going to last very long especially with new entrants like Grown Rogue, but you can model out the potential of New Jersey and one can come up with some eye-popping cash flow and free cash flow numbers once the company gets up and running in New Jersey.

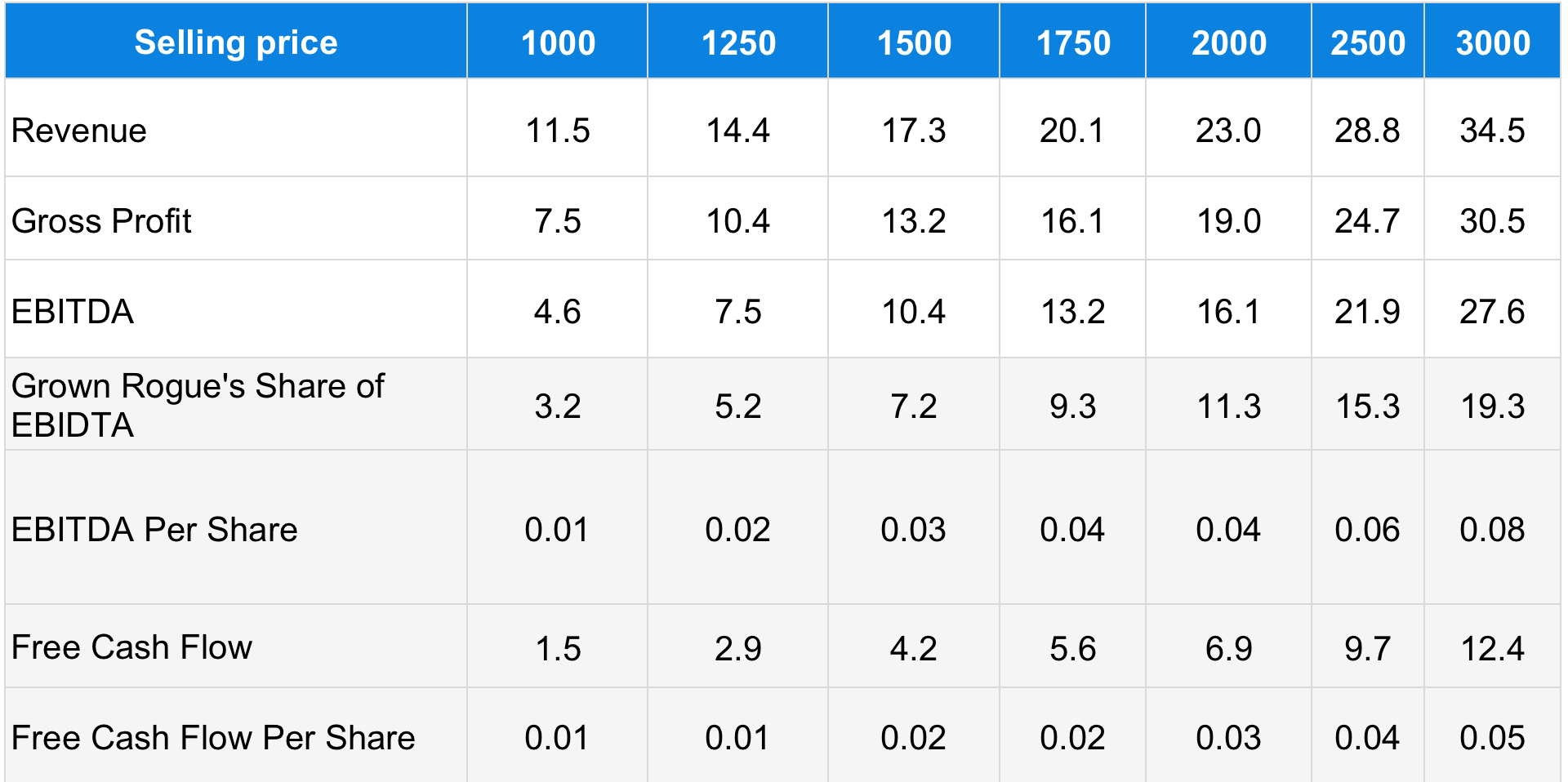

At $1500 wholesale pricing (50% less than current pricing), Grown Rogue should earn $7.2 million from just the state of New Jersey. The fully diluted market cap is around $62 million, meaning that Grown Rogue trades at less than 9 times EBITDA just from New Jersey once it is fully operational and ten times free cash flow.

But this doesn’t show just how undervalued it is because you then have to add in the estimated $10 million in EBITDA they should do next year from Oregon and Michigan and then add in their royalty from their strategic partnership with Goodness Growth in Maryland and Minnesota. I think this means the company should exit 2024 earning $20-$25 million in EBITDA, $10 million in FCF, growing at triple-digit rates.

But again, this might not even explain just how undervalued Grown Rogue is because the company is pursuing the same opportunity in multiple other states. For $4-$6 million, the company can enter a limited license state and become a craft cultivator and create cash flow streams of $7-$11 million at $1500-$2000 pricing, or $5 to $7 million at much more conservative pricing assumptions (see chart above).

Grown Rogue is an investor’s dream. It is a company with demonstrated operational and cost advantages that has a long reinvestment runway with extremely high returns on invested capital. In fact, in a schedule 3 world with some financial protections from SAFER Banking, this is a lender or a private equity firm’s dream investment.

There is no better investment than one that only has to lather, rinse and repeat over and over again.

I believe Grown Rogue can keep adding states and get to at least $50 million in EBITDA and $20-$25 million in free cash flow in the next few years and that the company should be worth more than $500 million.

Even better, if I’m a tobacco company or wine and spirits company looking to enter the industry, I can easily see how much capital has been lit on fire and how few know or understand the basic blocking and tackling of cannabis cultivation. What is the strategic value of a Grown Rogue to an acquirer or potential partner? This is why I could see Grown Rogue potentially being worth upwards of a $1 billion. Not bad potential for a $60 million fully diluted market cap.

For the larger Multi-State Operators (MSOs), Grown Rogue’s entry into the lucrative New Jersey market is not great news. Investors in any of the big operators should rightfully be concerned that a low-cost operator with superior quality is entering the most profitable and most protected market. How much does New Jersey represent of the large MSOs cash flow and profitability? What would happen if pricing fell to $1500 or lower like other markets have and what happens if Grown Rogue enters those other protected limited license markets as well?

And yet, no one is researching Grown Rogue, no one is studying the company or talking to management when what this small company does has profound implications for the larger publicly traded companies.

New Jersey going Rogue is not only very important to Grown Rogue, but also important for the industry, and I expect Grown Rogue to add several more limited license states in the future because consumers love great flower at great prices and the returns are just so high for the company. Grown Rogue is already one of the fastest growing cannabis companies out there and now growth is about to take a step function higher. The formula of taking its great quality flower at a great price to the rest of the country should delight consumers and investors alike.