Turning the Lights On

Grown Rogue’s Capacity Utilization is only at 42% Right Now

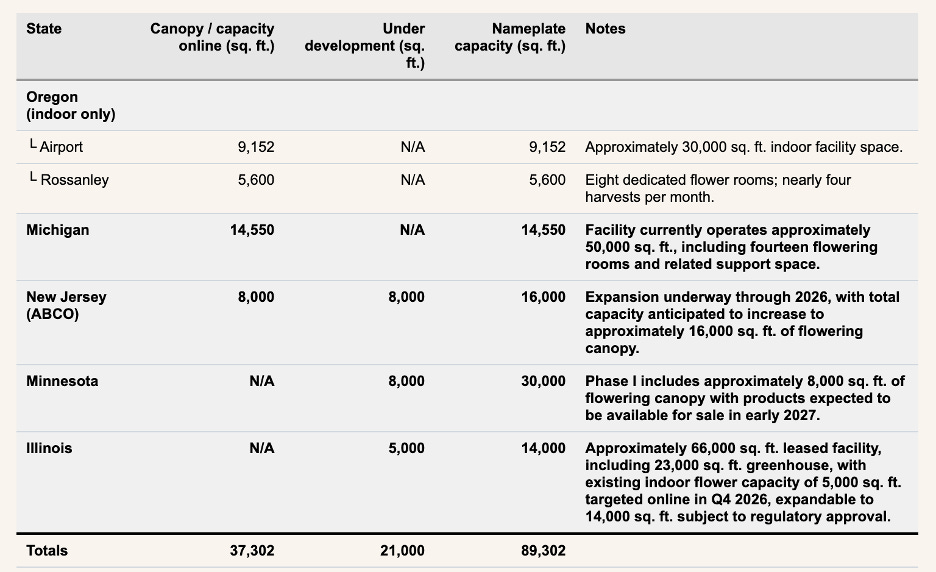

The following table tells a remarkable story about Grown Rogue (OTC: GRUSF):

Investors looking at Grown Rogue (GRUSF) see the surface-level numbers and move on. $32M in revenue. $5.4M in Adjusted EBITDA.

In our opinion, that’s the wrong way to look at the company.

Grown Rogue is licensed across five states - Oregon, Michigan, New Jersey, Illinois, and Minnesota - but today it is using barely 42% of its total production capacity. Two of those five states haven’t produced a single pound of flower. A third state is still at half its capacity. The company has been spending ahead of these opportunities and have yet to see the returns.

The business investors see today is a half-built machine. The question isn’t “what does Grown Rogue earn?” It’s “what does Grown Rogue earn when the lights are on in every room?”

The Capacity Math

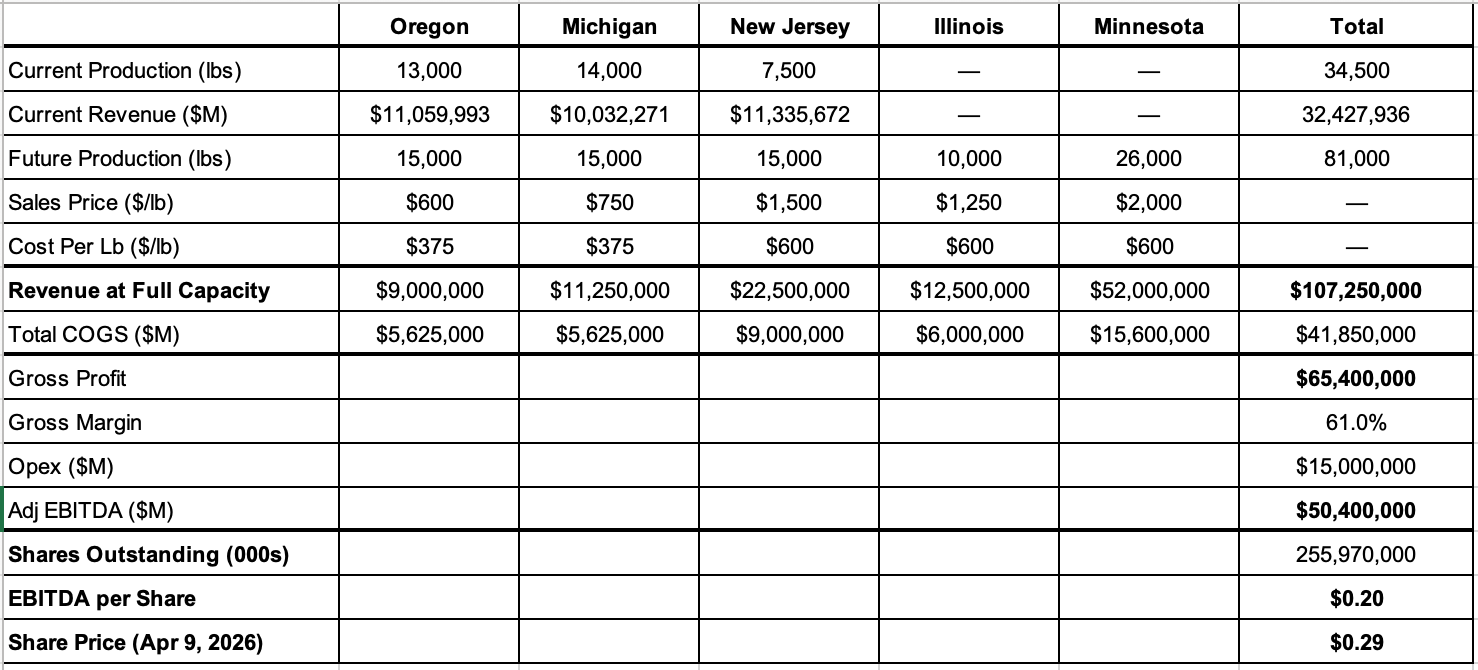

Here’s the state-by-state breakdown. Current production reflects FY 2025 actuals. Full capacity reflects licensed nameplate across all five facilities. Even at reasonably conservative prices, and an increase in current operating expenses, the company’s economics are very attractive and are the reason the company is now guiding to returns on incremental invested capital of 75%.

$107M in revenue. $65.4M in gross profit — a 61% gross margin. And $50.4M in adjusted EBITDA or $0.20 per share.

That is more than a 3X increase in revenue, and a 10X increase in adjusted EBITDA from where the company sits today.

And remember, the pricing assumptions should be conservative. Minnesota as a market is likely to be supply constrained for years, according to Vireo CEO Jon Mazarakis. A private operator recently said they expect to be “sold out for the foreseeable future.” The state of Minnesota itself estimates that an additional 1 million square feet of cultivation will be needed to satisfy demand. We believe that pricing is likely to remain high for several years.

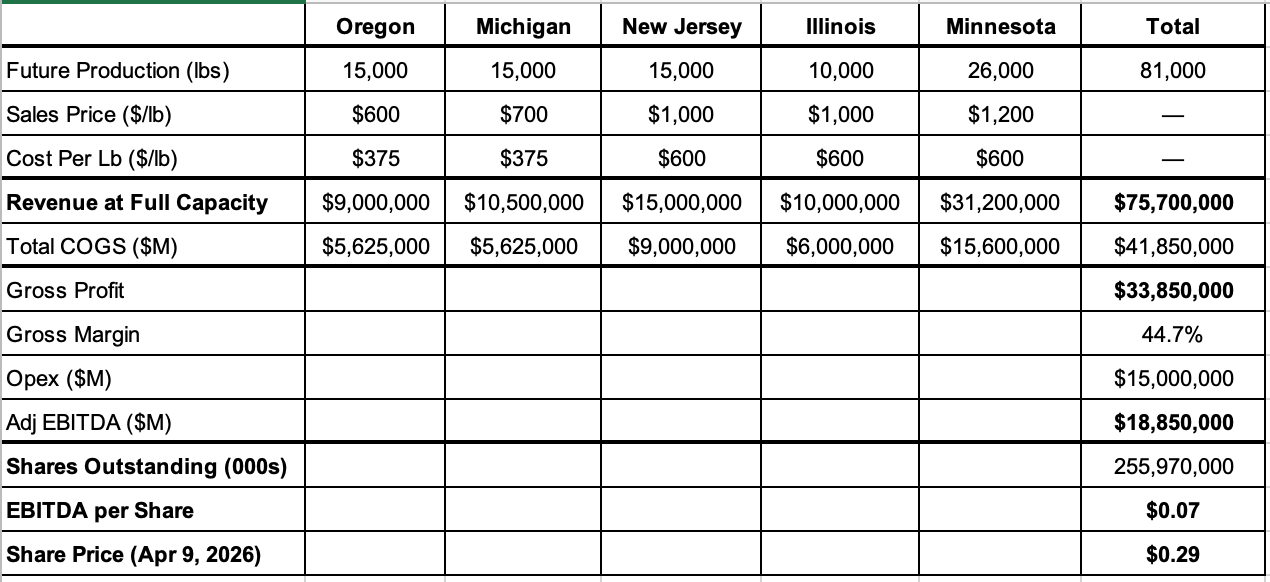

But even if we got draconian and assumed tough pricing in all markets including Minnesota, this is what Grown Rogue looks like at full capacity, and as you can see the company is still quite profitable.

It has been painfully hard to be patient as Grown Rogue has retraced its big advance and has been under constant selling pressure from funds shutting down and few willing to do any work on the underlying unit level economics. All the while, Oregon and Michigan experienced a brutal price decline and New Jersey took longer than expected to fully activate.

But the wait is almost over. The final phase of the New Jersey facility is under construction and the facility will soon be at full capacity. Illinois and Minnesota are in active development, with first harvests expected to start contributing to 2026 and ramp through 2027.

The company is turning the lights on a lot more cultivation capacity and come this time next year; Grown Rogue should be a substantially larger and a much more profitable company.

At today’s valuation, the market is pricing in what Grown Rogue earns at 42% utilization. It is not pricing in what the company earns when every cultivation room is running. That gap between $5M in EBITDA and $50M in EBITDA is the opportunity.

P.S. If you would like to play around with the assumptions made in this post, click on the link below and you can play around with cost and sales assumptions yourself. As always please so your own due diligence and rely on your research.