Forget Bitcoin, California Has Weed!

Forget Bitcoin, California Has Weed!

Just How Capital Starved is the Cannabis Industry?

I wasn’t planning on writing another post this week, but then I saw this.

A California cannabis company called Statehouse, which is trying to turn it’s operations around and restructure, cited in its regulatory document that it was selling a dispensary for cannabis flower and not cash.

While this transaction may be the result of a related party transaction, or two related entities transacting between each other (Thanks Lester Black), this is a really fun illustration of just how little capital exists in cannabis, especially in California.

Why is this important? Because it is actually really bullish for the surviving companies in cannabis and in California.

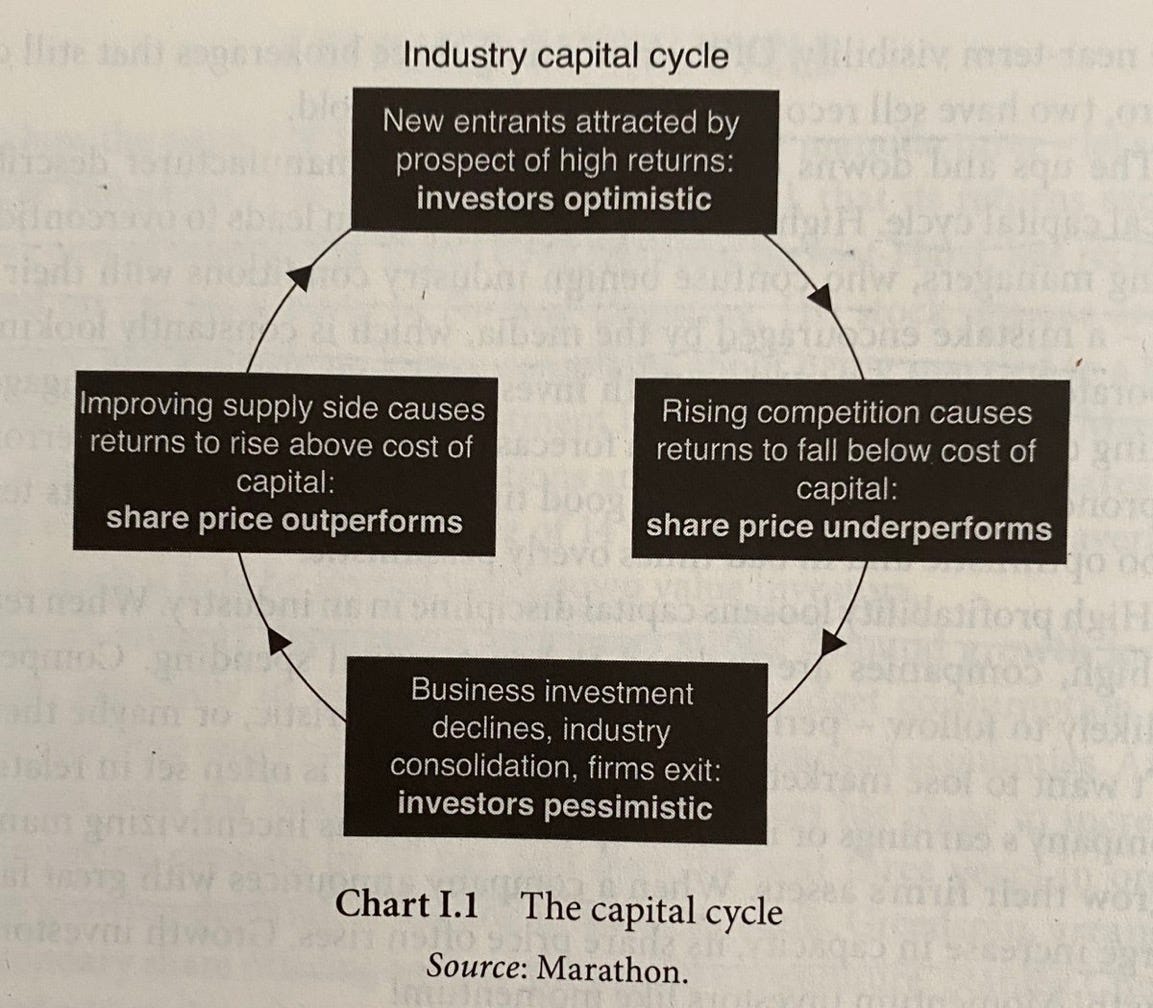

Capital Returns is an excellent book, which studies what happens when industries have either too much capital or are starved for capital. It turns out that when the capital spigot turns off and supply dries up, returns for the remaining companies that survive are outsized.

There is a simple and wonderful Twitter thread about this book for those who don’t want to read it here:

Brandon Beylo’s summary of Capital Returns

And we are seeing this play out in California. I heard from one of the larger private California cultivators yesterday that there is no excess supply of cannabis from Croptober outdoor production and that flower prices are firm when they should be weak. This operator expects prices to rise through spring as there simply is no supply to meet demand. Exactly what you would expect from an industry starved of capital.

California and the overall cannabis industry is rapidly rationalizing. Inefficient, poorly run operators are falling away and the end result should be wonderful returns for the remaining players. This is why I have written so extensively about California and Glass House (OTC: GLASF). It is also why I invested in Garden Society.

If history repeats itself, the fact that cannabis companies have to be paid in weed could not be more bullish and is one hell of a signpost of what is to come.